A Trade I Loved That DIDN'T Work

The good trade, bad beat story

The overwhelming tendency in our socially networked world is to glamorise and to show the good from the bad. Our online lives are curated galleries of triumph, with struggles swept aside.

Let’s be honest—we have all been guilty of posting some wins.

In trading, you always deal with uncertainty in a probabilistic game.

Some trades are good and they work.

Other trades are poorly thought out and reckless.

But there lies a space where you can do all the preparation, put yourself in a great position to capitalise, execute in the right places, and still lose! These are often tougher to accept than the reckless mistakes because you feel you did everything right.

I like to call these “good trade, bad beat”.

In this post, I share a trade this week that I loved as I went deeper into research. I was committed, but it just didn’t work out. The market just didn’t care. And to make money, we need the market to take an interest and for major players to act. This is outside of our control.

Let’s turn to the trade in question….

Biotechs hammered on the appointment of a new FDA head

On Tuesday 5th May, US Biotechs were routed as Dr Vinay Prasad was nominated as the head of the FDA’s CBER division. This division is responsible for regulating vaccines, cell and gene therapies, and blood-derived products.

The market took a view with the XBI, S&P Biotech ETF, falling -6.6%.

Prasad’s stance on COVID-19 vaccines and the broader drug approval process was perceived as anti-industry. More specifically, his views can be summarised as:

Supportive of stricter regulations;

Opposed to accelerated pathways and high-cost drugs or devices;

Demanding evidence of clinically meaningful endpoints (i.e. survival or quality of life outcomes) rather than surrogate end points such as biomarkers or response rates.

His appointment came as a surprise. Moderna fell -12.3% and was the weakest name on the SPX. Other names in Biotech land that were smoked included QURE -27.8%, SRPT -26.6%, XNCR -21.1%, and VRTX -10%. These are vicious moves for billion-dollar market cap companies.

XBI Daily:

These repercussions and sentiment were likely to have a meaningful impact on ASX-listed biotech and pharma companies.

What's the trade?

A discretionary trader’s core strength lies in piecing together multiple variables like a jigsaw to build conviction and size up the trade accordingly.

This is not an exact science. More often than not, you can’t quantify the specific impact on a company or its future probability. You are delving into the realm of forecasting, which is fraught with unknowns and uncertainty. As Howard Marks says in his latest memo:

if we insist on achieving certainty or even confidence as a precondition for action, we’ll be frozen into inaction

My view is to do the work, build a thesis, wait for clear price action and your systems as a reason to enter, and then be prepared to throw it all away. Strong conviction, lightly held.

In this example, there were multiple stocks with possible exposure:

CSL: vaccine and blood-derived products. No doubt has some well-established vaccines that would be very unlikely to change, but also note some 10% of its business is exposed to developing therapies for rare diseases (Haemophilia).

MSB: cell therapy assets. Ryconcil was recently approved, but 60% of its valuation is for unproven drugs for Cardiac failure and disc repair. Its drugs are also soooo expensive > $1.5m targeting an addressable market of 300 patients a year.

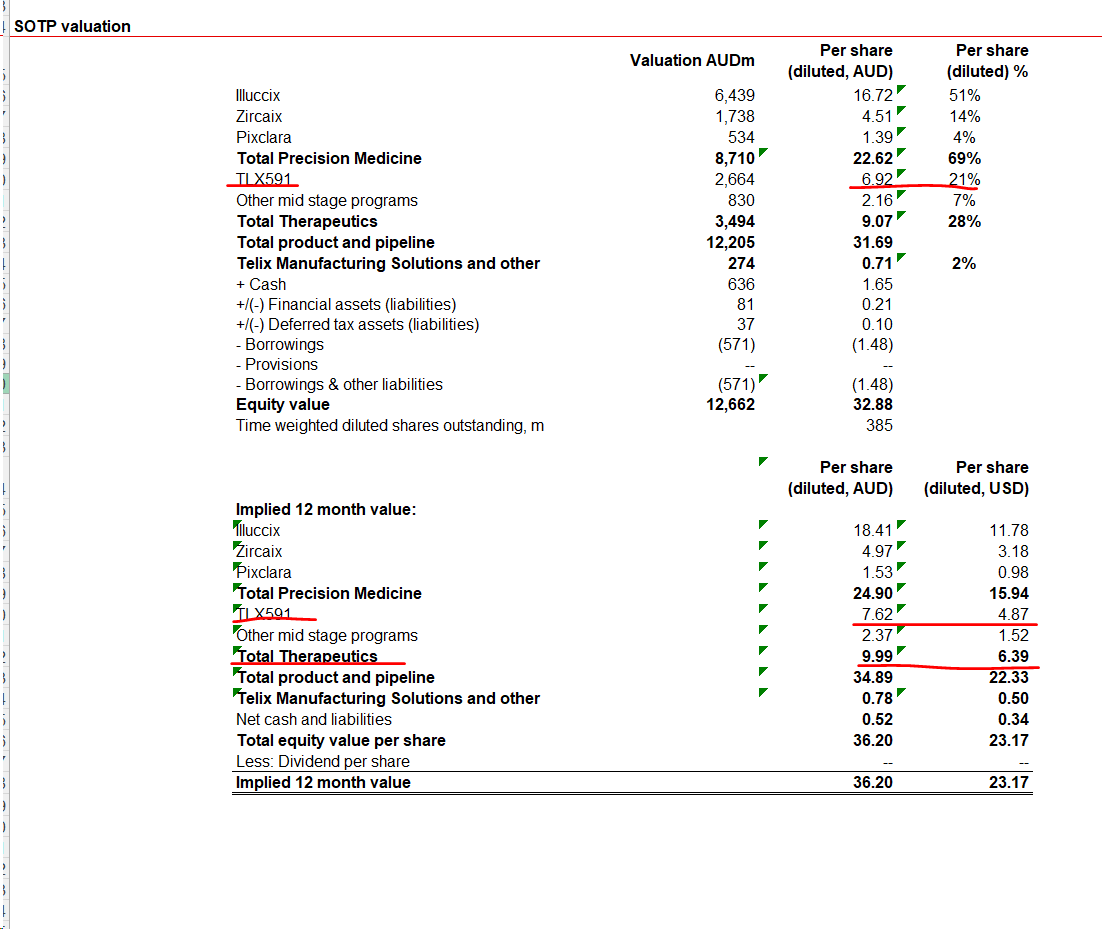

TLX: diagnostic assets, but 28% of its valuation is for therapeutics in various FDA phases, such as TLX591.

CU6: The TLX minnow is developing imaging and drugs for prostate cancer.

Other stocks exposed but with no liquidity or borrow include IMM, CYP, and ALA.

TLX valuation

MSB valuation

CSL valuation

Are these products suddenly zero? Of course not - but investors may question their time to market, the increased scrutiny, and the funding that will be needed vs payoff.

Furthermore, sentiment in the Australian biotech landscape has been knocked to pieces after the collapse of OPT, which caught out the likes of Regal.

This trade was very hard to quantify BUT there was an enormous amount of potential negative read across. It was also the kind of catalyst that would not necessarily be front and centre amongst traders. This could provide more edge as non-obvious and less crowded early.

Execution

What follows are my trade executions and notes.

MSB:

The ADRs closed at $1.68 equivalent on huge volume. This was the initial fair value. My thesis was that I wanted to see a sustained hold below this price and a true break as confirmation.

I entered a starter on the open and then more as the 1.68 level failed to lift. I could have been more patient early on, but I wanted to participate and watch.

The early action was whippy but RVOL was building and a seller was capping. There is finally volume into the 165 bid, and we break. If this were a genuine new leg lower, this was the spot. The potential target was into previous lows down at 150s. However, frustratingly, we cant hold below and squeeze back up. I take most of my stops.

Why not stop everything? It was a pure bias. I wanted to give the trade more time, but this invariably leads to more slippage.

Full size loss at close would have been -6.6k so I did outperform by taking those stops. Still room for improvement to take it all off when wrong- you can always get back in.

Keep reading with a 7-day free trial

Subscribe to Baytrading: Insights from an equities day-trader to keep reading this post and get 7 days of free access to the full post archives.