Reporting season has been and gone. In the aftermath, I felt drained and scattered despite the best intentions.

However, now that the dust has settled, it is important to reflect and learn. You've paid the tuition—don’t leave without the lesson. It will come around again so it is important to close the loop.

My original game plan was detailed here. This was a solid roadmap for me based on the work of previous cycles. Parts of the approach were effective, but some underperformance might be linked to shifting market dynamics and the sharp global sell-off in the second half. Furthermore, the quality of my application declined due to external factors. Reporting season will punish you for any shortcuts taken.

These are just excuses. What is important is investigating new strategies and solutions if the current ones are not working. That is a key component of the growth mindset.

There were certainly many great opportunities to dissect. The most interesting aspect was seeing strong follow-through after the opening in several gap-up plays on reporting day. Shorts also saw sharp sell-offs.

From UBS:

“February results in fact saw unprecedented share price volatility on result day with average intraday swings of 7%.”

In this newsletter, I expand on what I learned with some reflections and underlying data. This will frame adjustments to my process for next time. I hope this offers some fresh perspectives to integrate into your strategy when August rolls around.

Observations

→Day 1 plays worked

I have a love-hate relationship with trading reporting names on Day 1.

There is no doubt a huge opportunity in these setups BUT they also come with increased efficiency and increased slippage when wrong. A few bad beats can set you off course. These plays are best suited to traders with strong match and order book skills, shorter timeframe horizons, and scalping out quickly into extended moves. The key is filtering and picking the right battles.

However, every so often there is also a bigger trend in time and price. You have to be willing to accept the risk and the increased variance around the open to put yourself in a position to capture this reward.

This February, several stocks trended strongly to fit this profile. Some moves were quick and sharp such as CTD or HUB, whilst A2M and MPL climbed in a more measured way.

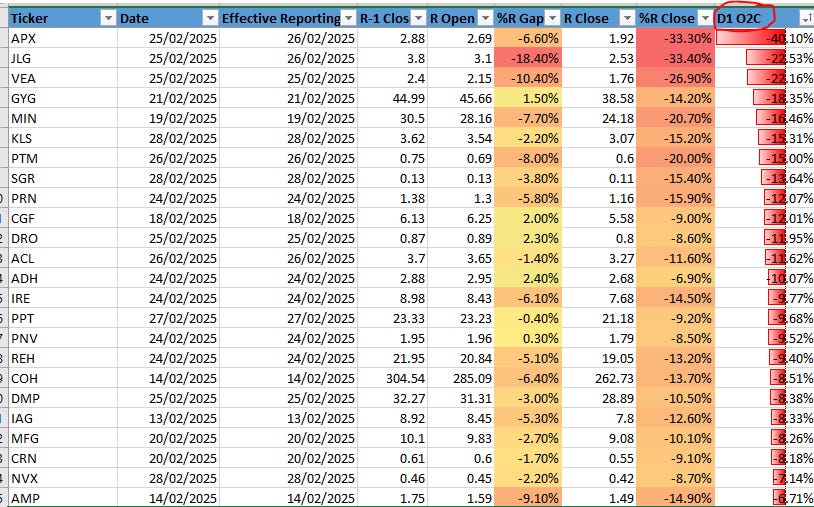

Here are some of the biggest open-to-close % winners:

(R = reporting day; D1 O2C = Day 1 open to close)

Big gaps are often a red flag as they show the market is across the catalyst, the EV is reduced, and there is an increased chance of mean-reversion or a “trap” if joining. The intraday trend performance for extreme gaps was certainly mixed but missing the open would have cut you out of many potential winners.

Here is the data sorted by the size of the gap:

I can't remember a time when so many Day 1 setups moved so cleanly in the direction of the gap, both up and down.

No doubt there is a lot of hindsight at play. Many of the stocks cited above have poor liquidity and are thinly traded around the open. Tickers such as AD8, ADH, ARB, ASB, DTL, IMD, KGN, KLS, MMS, MND, NAN, NEU, NHF, OML, PRN and REH all traded less than $250k on the open. This is not a scalable strategy for many.

However, what about stocks that did meet liquidity thresholds? Examples of winners included APX, A2M, AMP, BEN, BSL, CHC, COH, CTD, HUB, HLI, IAG, MPL, MIN, TLX, VEA and ZIP. There was money to be made here both long and short.

It is clear to me that this price behavior cannot be explained by the magnitude of the catalyst alone. Some of these stocks opened with a much bigger gap than the news delta indicated, yet they continued to trend. Several other forces include:

Lack of resting liquidity on the market post-open

Denomination of the security

Positioning in a bull market driven by passive money

Stale earnings estimates

UBS goes as far as to view this dynamic as a largely structural shift.

After witnessing the success of these setups, I adapted to put up a drive in MPL right at the end of the month. Better late than never.

Going forward, I will better explore the factors cited and incorporate them into my models. Having a Day 1 system can add meaningful alpha but it is important to recognise that there is so much randomness at play.

→Shorts also worked

Bears got paid.

Stocks were primed for perfection and any miss seemed to get punished. This was different from past cycles where the market tends to look through and give the big picture the benefit of the doubt. The broader sell-off and weak underlying conditions also seemed to contribute.

Examples of sharp moves to the downside included AMP, APX, BEN, CGF, COH, IAG, JLG, MIN, and VEA.

Traditionally I have found shorts to be high variance. Each example is specific and has its unique circumstances. As a basket, the performance data is terrible.

I stayed clear and in doing so, missed out on some great opportunities.

The right approach probably lies somewhere in the middle. Have no self-limiting beliefs and instead work on reverse engineering the examples and variables. Reduce size but be prepared to shift gears in real time in a see-it moment.

All it takes is one good trade to make the entire month. Just see @_findingmyedge with his incredible APX trade.

→Momentum drift was mixed

More mechanical systems looking to take advantage of momentum and revisions in the following days had mixed results.

Following a strong close on Day 1, the largest upward drifts on Day 2 came from A2M, AD8, APA, BAP, CTD, DHG, HLI, MGR, NAN, QBE, SGH, TLX, TPW, and VNT.

What challenged me was how the next day’s gap left little room to chase new setups. A number of these stocks received broker upgrades and quickly priced the new information.

Furthermore, several names failed to follow through and instead experienced moves to the downside despite a positive close AND consensus revisions higher. These stocks included 360, ABB, ANN, ARB, BGA, BSL, COL, JDO, HMC, NCK, MP1, NHF, and WOR.

All in all, I took my share of the good and bad amongst these setups. As the market deteriorated in the back half of February, sentiment softened—never a good backdrop for momentum.

→Price action is the truth

The only thing that gets you paid is the price action.

You can do all the work in the world on the catalyst and build conviction. You can backtest strategies to build a solid edge. But when a stock is not acting right, you must be prepared to cut it and accept what IS happening.

This message still hasn’t fully sunk in. I took heavy losses in ABB, AGL, and BGA by building conviction in the news and my strategy but ignoring the clear selling pressure that signaled I was wrong.

Taking outsize losses during the Earnings season undoes so much of the good work. It reduces confidence and capital for the next opportunity.

The correct mantra should be - “strong conviction, lightly held”.

The advantage of being a short-term trader is having fast feet and being able to adapt quickly. Don’t blur the lines.

Improvements

Based on the lessons and data, there are some clear adjustments to make going forward:

Add max adverse excursion stops: despite best intentions, I don’t feel comfortable as a fully systematic trader. Over a large sample size, holding positions from open to close is the best exit for a core strategy. This comes with an increased standard deviation. To be able to execute this effectively, you need to be trading in a position of strength. Recent results and general market feedback have placed me in the opposite situation. The best candidates should gap and go. They should be hard to get into. Any position that immediately trades > 2% against me rarely comes back. Examples on the second day included ABB long, BGA long, PME long, and JLG short. Adding a % stop may not make statistical sense, but it fits my profile.

Build a stronger Day 1 system: one season doesn’t make a trend but there is clearly significant opportunity. The solution is not to ignore these plays but to build more robust criteria, filters, and rules. Spend less time analyzing the news itself and more time on important parameters. Some key insights i) Add tools to focus on stocks with liquidity and range ii) Analyze order book depth and resting liquidity profiles iii) Tailor entry and exit rules based on denomination iv) Study slippage

Incorporate AI: there are lots of potential projects to better manage the workload. Comparing announcements to consensus; highlighting keywords and phrases; and summarising conference calls. Capped by imagination here.

Conclusion

Earnings season always has its unique characteristics and patterns - this was no different.

A defining feature was witnessing poor liquidity on the market post the match, particularly in the higher denomination stocks. You either joined the gap and got paid, or you were left on the sidelines.

Having said that, there were some exceptions to this rule which offered a very tradeable and liquid move- APX. You just had to put yourself in a position to capitalise.

After so much volatility, it is important to reset and let the dust settle. Just don’t lose the opportunity to learn and make new plans for next season.

Keep reading with a 7-day free trial

Subscribe to Baytrading: Insights from an equities day-trader to keep reading this post and get 7 days of free access to the full post archives.